News

Below are some snippets, pearls of wisdom and random thoughts from the team. Nothing is personal advice nor should it be relied on when conducting your affairs. You should seek advice on any of the below information before acting on it. If anything piques your interest please get in touch and we can elaborate some more!

How to use a mortgage offset account to save tax - 17 June 2019

Generally speaking you will pay tax on any interest you earn on savings in your bank account. This includes accounts set up for social events and the like so it pays to be aware of where you've got bank accounts. Now if you've got a mortgage you can often obtain a linked bank account that offsets the loan for however much is in there (hence the name 'offset' account). As an example it works something like this:

- Mortgage amount: $300,000

- Savings in offset account: $50,000

- Amount that interest is charged on $250,000 ($300,000 less $50,000)

If the $50,000 was sitting in a savings account this would be earning interest and the ATO would be taking a portion of it as tax, depending on your other income. However, if you're saving your mortgage interest rate, which is almost certainly higher than a savings account rate, you're effectively earning that amount of interest tax-free!

If you're financially disciplined and have the ability to keep all surplus income in this account without touching it, the savings can really add up. Think of $20,000 kept in an offset account, for someone earning $37,000 per annum. If the mortgage rate of interest was 4.5% then this person would be saving $900 of interest per year PLUS almost $300 in tax. All for picking up the phone to the bank.

For sole traders that keep income tax and GST payments aside for tax and BAS time if these payments are kept in an offset account it can boost these savings further.

There are a few caveats on this, including potentially higher fees and that the rates of interest can be higher but I know personally that my bank have written off the annual fees on my account and my rate of interest is incredibly competitive. It may be worth a call to the bank to see how it can work for you.

Looking for an investment property? The market may be turning - 3 June 2019

We have a lot of clients either holding investment properties or looking to purchase one. Where the market is at is anyone's guess, with some pundits suggesting there's still more cooling to happen in the 2019 calendar year and others indicating we may be at the bottom. But where is the future of property prices? Will we see years of stagnant prices like we did in Sydney and Melbourne in the post-GFC period? After 11 months of stagnant growth so far in those capital cities it looks like capital growth is off the cards for a little while.

One interesting article I've read today paints a slightly optimistic view of the current market and, although lacking in any soothsayer-like predictions, still makes an interesting read. What does it mean for the Newcastle market, where most of our clients reside? Well we're largely insulated from Sydney and Melbourne factors but there's still a localised effect here. While some suburbs are seeing falls others are seeing their strong prices being pretty robust.

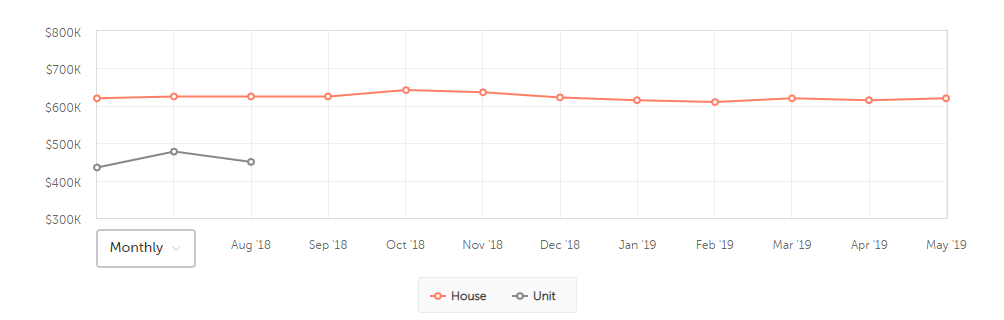

As an interesting takeaway have a look at the graph below. This shows the median house price for the suburb where we're located, Kotara, over the past 9 months or so. Unit prices are missing but the graph has a telling story for house prices: nil growth means prices aren't keeping up with inflation. Throw in low rental yields and take out rates, servicing of debt and other costs and property isn't looking as rosy as it has in the past.

Single Touch Payroll Update - 27 May 2019

The ATO are on track to roll out Single Touch Payroll on 1 July to all employers (previously this was only those employers with more than 20 staff). Employers with less than 20 employees can already opt-in to the process and we've been recommending our clients do this to make any transition come 30 June relatively seamless. It's an easy process - notify the ATO of your software ID (if you're using software) then a couple of clicks within that software and you're pretty well done. As with anything there can be a couple of extra boxes to tick but we can handle those for you pretty easily.

If you're not using payroll software now is the time to get on board. From a business standpoint paying employees is much easier when it's handled by software, the reporting options give you good insights and they report directly to the ATO to keep you Single Touch Payroll compliant. There are some good low-cost options out there that we can assist with.

Record Keeping for CGT purposes - 23 May 2019

You need to keep records for all of your tax affairs for 5 years from the date you lodge your tax return. There are some exceptions to this, however 5 years is the minimum.

If you hold shares, an investment property or other assets that can make a gain or loss for tax purposes, you'll need to keep records that establish the following for the sale and purchase:

- The purchase and sale price

- Costs associated with the purchase/sale (broker's fees, agent's fees, stamp duty etc)

- The purchase and sale date

- The parties involved

There are other considerations such as selling jointly owned assets and selling shares where dividends have been reinvested so it pays to keep all documentation for these assets.

The ATO have some good guidance on their site, listed here.

Renting out a room on Airbnb or thinking about it? See below for the taxation implications

A growing number of clients are renting out rooms or their whole houses on sharing sites, primarily Airbnb. While this is a great way of earning some additional revenue for space that would otherwise be going unutilised, there are taxation implications in relation to the income generated, as well as the expenses incurred in relation to the room.

The boring stuff

Very generally speaking, expenses incurred in generating assessable income can be deducted against that income. For salaried employees this would include the costs of washing a work uniform, purchasing occupation-specific equipment for use at work, or the costs associated with travelling for work where these aren’t reimbursed by your employer.

So how does this affect me renting my room out?

The income generated from Airbnb or other sharing sites needs to be declared to the ATO on your tax return. If you own or rent your property as joint tenants or tenants in common, the income will need to be split accordingly.

The expenses incurred in renting the room out can be claimed against the income. After all, if you hadn’t incurred those outgoings, you wouldn’t be able to generate the income and the taxman wouldn’t be able to collect his share.

Right, but what can I claim?

The ATO are very specific on what you can and can’t claim. Simply speaking, you can claim 100% of the expenses directly incurred such as Airbnb fees. Seeing as rooms rented are only sporadically used to generate income, the remainder of expenses will almost always have a personal usage component and should therefore be apportioned accordingly.

The following can be deducted against your income:

-Airbnb/sharing service fees – 100%

-Cleaning costs – 100% if specific to the room being rented, otherwise a percentage

-Council rates – a proportion

-Interest on loan for the property – a proportion

-Electricity and gas – a proportion

-Property insurance – a proportion

Woo hoo! Free money! So how do I allocate a proportion?

This is where it gets a bit tricky. You’ll need to work out and document an appropriate deductible portion to claim on your return based on the dates the room/house was rented, the floor space of the room/s rented if not the whole house, and the usage of the room when it’s not rented.

Expenses associated with common areas such as the lounge room are also deductible, but must be apportioned in the same fashion.

The ATO have a good method for calculating this on their website, which can be found here: https://goo.gl/x6QhgF

Anything else?

There are capital gains implications when it comes time to sell the house which need to be considered as well. It gets a bit more in depth here, so if you want to know more grab the phone and give us a call, email us or pop in and say hi. We’re next door to a great cafe (Shoutout to The Letter Q!) so would be happy to grab a coffee and chat about it.

How to stay on the right side of the ATO when it comes to Christmas Parties and Christmas gifts

It’s that time of the year when many employers thank their staff for a job well done throughout the year at the annual Christmas Party. Debauchery jokes aside there are a number of consequences for the employer depending on the amount spent, who attends and the location of the party.

In short, there is no FBT liability provided the benefit per head is less than $300.00. However, this means that the expense is not deductible for income tax purposes. This $300.00 is not just for Christmas Parties, it’s the ATO’s allowance for incidental benefits that are provided from time to time and are not regular.

The costs associated with entertaining clients are not subject to FBT however again, are not tax deductible.

The costs of providing a Christmas Party is deductible when FBT is paid.

If the party is held on the business premises then it may be exempt from FBT; those held at a restaurant or other off-site location attract the FBT rules above.

As always, if you need a hand working this out prior to the party, please contact us using the website or call on 02 4952 3472 to discuss your circumstances further.